Industry Overview

The following abbreviations are used in this section:

| ASEAN | Association of Southeast Asian Nations |

| Canggih | Canggih Logistik Sdn Bhd (626528-V) |

| IILS | International ILS |

| ILS | Integrated logistics services |

| KLIA | Kuala Lumpur International Airport |

| Protégé Associates | Protégé Associates Sdn. Bhd. |

| Subsidiaries | XHTT, XHAE, Canggih and XHUF, collectively |

| XHAE | Xin Hwa Auto Engineering Sdn Bhd (659918-D) |

| XHH or Company | Xin Hwa Holdings Berhad (1032102-P) |

| XHTT | Xin Hwa Trading & Transport Sdn Bhd (447397-X) |

| XHUF | XH Universal Forwarding Sdn Bhd (957938-M) |

Technical References

| Prime mover | A vehicle that provides the motive power to haul a trailer |

Logistics is widely known as the act of managing the efficient and cost effective flow and storage of goods (such as raw materials, in-process stocks and finished goods) and related information from the point of origin to the point of consumption for customers covering inbound, outbound, internal and external movements as well as reverse product flows.

Logistics services can be divided into physical and non-physical activities. Physical activities mainly comprise transport and storage activities while non-physical activities consist of activities such as designing supply chain, selecting contractors and negotiating on freightage. There are various activities involved in the logistics process flow namely procurement, inbound logistics, production operations, outbound logistics, sales and marketing and after-sales services.

Figure 1 : Activities in the Logistics Process Flow

Source: Protégé Associates

The flow of information in activities of logistics services can also be from the point of destination to the point of origin. This typically occurs in reverse logistics that involves all activities after the point of sale. For example, a defective product under a product warranty period may be sent back to the manufacturer via the distributor – moving in reverse through the supply chain network.

In terms of industry structure, the logistics industry comprises of transport service providers and logistics service providers. Given that XHH, through its Subsidiary companies, is primarily involved in cargo (goods or produce transported by a vessel or vehicle) logistics by land, Protégé Associates will provide a write-up on the logistics industry in Malaysia involving cargo focusing mainly on road transport.

Figure 2: The Industry Structure of the Logistics Industry Notes:

Notes:

- 3PLs denotes third party logistics providers that provide multiple logistics services which are generally integrated or 'bundled' in nature for use by their customers;

- 4PLs denotes fourth party logistics providers that are generally established as a separate entity through long-term contract or joint venture between a primary customer and one or more partners to manage all aspects of the customer's supply chain; and

- ICT denotes information and communications technology

Through its Subsidiaries, XHH is a road transport operator involved in the transportation of goods or haulage operations on the road using goods vehicles such as trucks, prime movers and trailers and a logistics service provider that is involved in the provision of facilitation services, distribution services and ILS.

Facilitation service providers are involved in assisting and/or easing the logistical process flows. Examples of facilitation services providers are custom brokers, freight forwarders, consolidators, non-vessel operating common carriers, ship brokers and shipping agents.

Distribution service providers are involved in delivering of goods from the point of origin to the final consumers. The primary activities of distribution services are warehousing, transportation, inventory management and courier services (by domestic and regional distribution and courier companies).

ILS providers act as a 'one-stop centre' for their customers' logistic needs by being involved in various segments across the logistics value chain. 3PLs and 4PLs are typically providers of ILS.

A logistics company that provides integrated and door-to-door logistics services along the logistics value chain as a single entity on a regional or global scale is granted by the Malaysian Government an IILS status that allows it to expand its activities to ASEAN countries. A qualified logistics company with the IILS status will be issued with a Customs Agent Licence.

Protégé Associates is of the opinion that IILS Status companies have a wider geographical presence as compared to logistics companies that focus more on the Malaysian market such as XHH.

| Indicator | Measurement |

| 2014 Estimated Industry Size (Industry Revenue) | RM148.82 billion |

| 2014 Estimated Industry Growth Rate | 11.2% |

| 2019 Forecast Industry Size (Industry Revenue) | RM253.21 billion |

| Forecast Period (2014-2019) Industry Compound Annual Growth Rate ("CAGR") | 11.2% |

| 2014 Estimated Number of Industry Players | There are a total of more than 12,000 logistics industry players in Malaysia. Around 7,700 logistics industry players are directly involved in cargo transport by road. |

| 2015 Demand Conditions |

|

| 2015 Supply Conditions |

|

Source: Protégé Associates

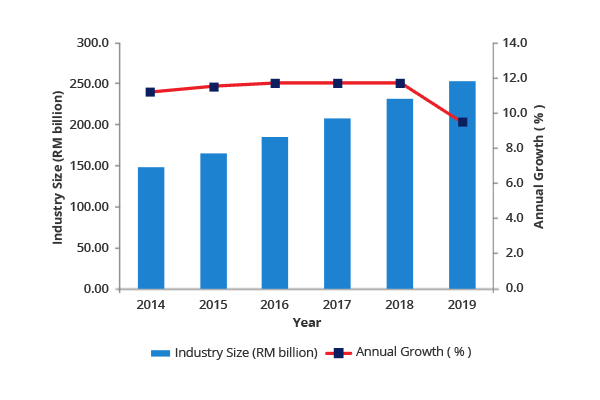

The logistics industry in Malaysia entered 2015 on a stronger footing as it managed to register a double digit growth for 2014. The logistics industry in Malaysia expanded by an estimated 11.2 percent from RM133.83 billion in 2013 to RM148.82 billion in 2014. The growth in the local logistics industry was largely attributed to the continuing expansion in the global and local economies. The growth in Malaysia's trade volume has also led to a rise in demand for transport and logistics services.

Figure 3: Historical, Estimated and Forecast Industry Size (Industry Revenue) of the Logistics Industry in Malaysia, 2014-2019 Notes:

Notes:

- CAGR (2014-2019) = 11.2 percent

- The base year is 2014

On a closer look at the road transport market within the logistics industry in Malaysia, the market grew by 4.3 percent to reach RM29.93 billion in 2014 as the expanding local economy has helped to drive the demand for road transport. Moving forward, the market size (market revenue) of the road transport market in Malaysia is expected to expand from RM29.93 billion in 2014 to RM37.33 billion in 2019 and register a CAGR of 4.5 percent.

Figure 4: Historical, Estimated and Forecast Market Size (Market Revenue) of the Road Transport Market in Malaysia, 2014-2019 Notes:

Notes:

- CAGR (2014-2019) = 4.5 percent

- The base year is 2014

The logistics industry in Malaysia is highly fragmented with the estimated presence of more than 12,000 industry players that are involved in various scopes of logistics activities in 2014. Logistics industry players in Malaysia are generally concentrated in key logistics spots such as:

- Johor (Pasir Gudang, Port of Tanjung Pelepas, Senai);

- Labuan;

- Malacca;

- Negeri Sembilan (Nilai);

- Pahang (Kuantan);

- Penang;

- Sabah (Kota Kinabalu);

- Sarawak (Bintulu, Kuching, Miri);

- Selangor (KLIA, Port Klang, Shah Alam); and

- Terengganu (Kemaman).

The logistics industry players in Malaysia can be distinctly divided into three types namely listed local, non-listed local and foreign-owned industry players.

Protégé Associates has also provided a closer look at the level of fragmentation involving logistics industry players in Malaysia that are competing with XHH in terms of cargo transport by road, storage and warehousing services as well as shipping and forwarding agencies services. It was estimated that there were around 7,700 industry players in Malaysia that were involved in cargo transport by road in 2014 with an estimated 15 percent of them based in Johor. Logistics industry players involved in cargo transport by road were mainly individual proprietorships and private limited companies. There were estimated to be around 250 logistics industry players in Malaysia that were involved in the provision of storage and warehousing services in 2014 with an estimated 5 percent of them based in Johor. These logistics industry players were mainly private limited companies. The value of fixed assets owned by these logistics industry players as at end of 2014 was estimated to be more than RM1.60 billion.

Lastly, the number of logistics industry players in Malaysia involved in shipping and forwarding agencies services in 2014 was estimated to be around 1,500. It was estimated that around 15 percent of them were operating in Johor. These logistics industry players were mainly private limited companies.

Source: Protégé AssociatesThe revenue generated by XHH for the financial year ended 31 December 2013 was RM97.9 million which is equivalent to 0.07 percent of the estimated industry size (industry revenue) of the logistics industry in Malaysia in 2013. The market share is derived from dividing XHH's revenue of RM97.9 million for the financial year ended 31 December 2013 with the industry size (industry revenue) of the logistics industry in Malaysia in 2013 which stood at RM133.83 billion. The estimated market share of the five industry players selected for comparison ranges from 0.05 percent to 0.23 percent – further reflecting the fragmented nature of the industry.

Figure 5: Estimated Market Share of Selected Industry Players in the Logistics Industry in Malaysia, 2013| Company Name | Financial Year Ended | Revenue (RM million) | Market Share (%) |

| Century Logistics Holdings Berhad | 31-12-2013 | 255.8 | 0.19 |

| Interway Transport Sdn Bhd | 31-12-2013 | 63.4 | 0.05 |

| Tanjong Express (M) Sdn Bhd | 31-12-2013 | 98.3 | 0.07 |

| Tiong Nam Logistics Holdings Berhad | 31-03-2013 | 308.0* | 0.23 |

| XHH | 31-12-2013 | 97.9 | 0.07 |

* Revenue generated from services rendered

- The list of selected industry players above is not exhaustive

- The above market shares only provide an indication and are not considered directly comparable due to the following reasons:

- The revenue of all industry players are not from the same financial year end

- The revenue may be at the group level

- Not all companies carry out activities which are completely similar to each other or in the same geographical area

- The market share of each industry player is calculated by dividing the revenue of each industry player in the financial year ended 2013 with the size of the logistics industry in Malaysia in 2013 which was RM133.83 billion

- The next financial year end for Konsortium Logistik Bhd ("Konsortium Logistik") after 31 December 2012 was 31 March 2014.

The revenue generated by XHH for the financial year ended 31 December 2014 was RM110.6 million which is equivalent to 0.07 percent of the estimated industry size (industry revenue) of the logistics industry in Malaysia in 2014. The market share is derived from dividing XHH's revenue of RM110.6 million for the financial year ended 31 December 2014 with the industry size (industry revenue) of the logistics industry in Malaysia in 2014 which is estimated to be RM148.82 billion.

Figure 6: Estimated Market Share of Selected Industry Players in the Logistics Industry in Malaysia, 2014| Company Name | Financial Year Ended | Revenue (RM million) | Market Share (%) |

| Century Logistics | 31-12-2014 | 275.2 | 0.18 |

| Konsortium Logistik | 31-03-2014 | 347.2 | 0.23 |

| Tiong Nam | 31-03-2014 | 345.3* | 0.23 |

| XHH | 31-12-2014 | 110.6 | 0.07 |

* Revenue generated from services rendered

- The list of selected industry players above is not exhaustive

- The market share of Interway Transport Sdn Bhd and Tanjong Express (M) Sdn Bhd are not provided as their financial figures for the financial year ended 2014 are not yet available

- The above market shares only provide an indication and are not considered directly comparable due to the following reasons:

- The revenue of all industry players are not from the same financial year end

- The revenue may be at the group level

- Not all companies carry out activities which are completely similar to each other or in the same geographical area

- The market share of each industry player is calculated by dividing the revenue of each industry player in the financial year ended 2014 with the size of the logistics industry in Malaysia in 2014 which is estimated to be RM148.82 billion.

XHH's revenue registered for the financial year ended 31 December 2014 is equivalent to 0.37 percent of the estimated market size (market revenue) of the road transport market in Malaysia in 2014. The market share is derived from dividing XHH's revenue of RM110.6 million for the financial year ended 31 December 2014 with the market size (market revenue) of the road transport market in Malaysia in 2014 which is estimated to be RM29.93 billion.

Demand and supply conditions refer to market factors that can positively or negatively affect future industry size (industry revenue) and growth by specifically altering demand or supply dynamics. These demand and supply factors can include trends, key developments or events that spur market expansion, leading to increase in sales or revenues, or developments that negatively affect market growth. The following figure depicts the demand and supply conditions affecting the value and growth of the logistics industry in Malaysia and highlighting the impact on the present industry situation in the country.

Figure 7: Demand and Supply Conditions Affecting the Logistics Industry in Malaysia, 2015| Condition | Type | Impact |

| On-going Implementation of Government Initiatives | Demand | + |

| Expansion in the Global and Local Economies | Demand | + |

| Changing Structure of Malaysia's Exports | Demand | + |

| A Very Broad Range of End-user Markets | Demand | + |

| The Growing Prominence of E-commerce | Demand | + |

| Encouraging Support from the Malaysian Government | Supply | + |

| A Strategic Logistics Hub with Business-friendly Logistics Ecosystem | Supply | + |

| Positive Developments in ICT Help to Support Growth | Supply | + |

| Weaker Oil Prices Ease Pressure on Cost of Operations | Supply | + |

| Intense Price Competition | Supply | - |

| Challenging Environment for the Hiring of Goods Vehicle Drivers and Relatively Low-skilled Workers | Supply | - |

| Vulnerability to Meteorological Changes and Natural Disasters | Supply | - |

| Vulnerability of Transportation Terminal Operations to Workers' Rights Activism, Strikes and Protests | Supply | - |

The logistics industry still plays a crucial role in today's supply chain management and transportation of physical cargo. In terms of transport services, one mode of transportation may not be an absolute substitute for another. Cargo may also be transported via a combination of different modes of transportation. The mode of choice for cargo shippers is dependent on various factors such as cost, capability, route and speed. Meanwhile, logistics services are still widely required to provide support to the principal transport mode(s). However, not every logistics services may be required. The extensiveness and/or choices of logistics services required are subject to various factors such as supply chain strategy, operating cost structure, the involvement of cross-border trades and etc.

On another note, it needs to be pointed out that the dematerialisation and electronic distribution of 'info-products' (via the Internet) may lead to a reduction in the volume of certain cargo movement. For examples, the direct delivery of products such as videos and software via the Internet rendered it unnecessary to engage transport and/or logistics services. Nevertheless, the reduction in the volume of the cargo movement due to such dematerialisation and electronic distribution is expected to be relatively small and exceeded by the vast potential cargo traffic generated by a wider sourcing of supplies through Internet trading.

Source: Protégé AssociatesThe logistics industry in Malaysia is projected to continue expanding during the 2015-2019 forecast period.

Figure 8: The Forecast Industry Size (Industry Revenue) of the Logistics Industry in Malaysia, 2015-2019 (Source: Protégé Associates)

(Source: Protégé Associates)The positive outlook on the demand for transport and logistics services in Malaysia stems mainly from the on-going implementation of government initiatives, expansion in the global and local economies, changing structure of Malaysia's exports, the presence of a very broad range of end-user markets and the growing prominence of e-commerce. The Malaysian Government is also bullish on the growth prospect of the overall volume of cargo transport.

On the supply side, although the industry is expected to be boosted by the encouraging support from the Malaysian Government, the position of Malaysia as a strategic logistics hub with business-friendly logistics ecosystem, positive developments in ICT that help to support growth and weaker oil prices that ease pressure on the cost of operations, it faces various challenges ahead. Intense price competition is expected to persist due to the high level of fragmentation. Besides that, the logistics industry in Malaysia is also expected to face a challenging environment for the hiring of goods vehicle drivers and relatively low-skilled workers. Its operations are also vulnerable to meteorological changes and natural disasters as well as any workers' rights activism, strikes and protests at transportation terminals.

Moving forward, the industry size (industry revenue) of the logistics industry in Malaysia is projected to expand from RM148.82 billion in 2014 to RM253.21 billion in 2019 and register a CAGR of 11.2 percent.

The local road transport market is also projected to register continuing growth from 2015 to 2019. The market size (market revenue) of the road transport market in Malaysia is projected to reach RM37.33 billion in 2019.

Figure 9: The Forecast Market Size (Market Revenue) of the Road Transport Market in Malaysia, 2015-2019 Source: Protégé Associates

Source: Protégé Associates